Goal 17

Partnerships for the goals

Debt is an important part of any financing strategy by both governments and private firms. From the point of view of financing sustainable development, the most important criteria for the long-term sustainability of debt obligations by public and private sector entities alike is that borrowing serves the purpose of increasing productive investment. If this is the case, increases in domestic income and export earnings will usually cover the servicing of outstanding debt obligations, given the average interest rate and maturity of the debt stock. But entirely manageable debt burdens under normal circumstances can still become a problem when a debtor economy is hit by severe shocks that are not under its control, such as, for example, a sharp fall in the international price of commodities that are an important part of its export basket.

A national debt, if it is not excessive, will be to us a national blessing. Hamilton, (1781)

Total external debt stocks in developing countries have increased markedly in the wake of the global financial crisis of 2007/08, with the steepest increases occurring in small island developing States, East Asia and the Pacific, Eastern Europe and Central Asia, and Latin America and the Caribbean.

This partially reverses a more positive trend that had seen considerable improvements in debt sustainability across developing regions as a result of strong overall growth performances in the period 2000-2008, coupled with the impact of large debt relief initiatives in the 1990s and early 2000s.

Until recently, the Bretton Woods InstitutionsThe Bretton Woods Institutions are the World Bank and IMF. They were set up at a meeting of 43 countries in Bretton Woods, New Hampshire, in July 1944.

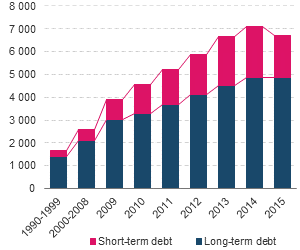

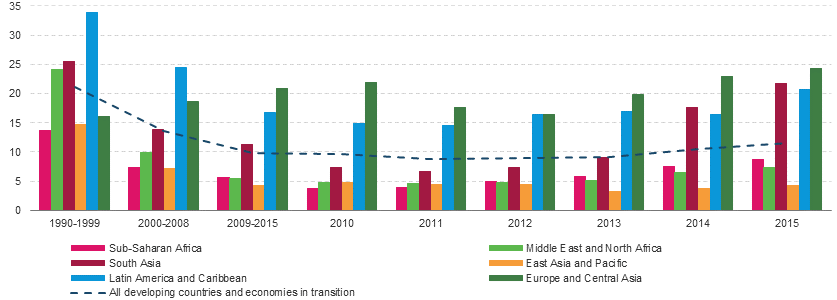

more have largely equated debt with external sovereign debt for the purposes of assessing debt sustainability, defined in non-technical terms as the ability to service a debt without the need for adjustments to the fiscal balance (IMF, 2011). This focuses primarily on short-term debt sustainability from the perspective of the creditor’s interest in the debtor’s ability to fully repay the debt. In the case of sovereign debtors borrowing abroad, an important way of assessing their repayment ability is to link their debt obligations to their capacity to generate export earnings. This is measured statistically as the ratio of debt service over exports. A fall in this ratio can result from increased export earnings, a reduction in debt servicing costs or a combination of both. Figure 17.8 shows that this ratio fell, for all developing countries on average (blue dotted line), throughout the 1990s and 2000s, signalling an improvement in debt sustainability. However, it has started to increase again since 2012.

In recent years, there has been growing recognition that debt sustainability in developing economies is facing a range of new challenges and vulnerabilities (Akyüz, 2014). Thus, the composition of developing countries’ debt has undergone substantial changes that affect its sustainability in different ways. As can be seen in figure 17.8, the share of short-term in total external debt of developing countries has increased since 2014, reaching 25 per cent in 2014. Short-term debt carries a higher roll-over risk than long-term debt, and increases an economy’s exposure to global interest rate changes.

In emerging economies, the corporate external debt of non-financial companies has more than quadrupled, from US$4 trillion in 2004 to US$18 trillion in 2014 (IMF, 2015). Although bank syndicated loans are still the largest component of this debt, the share of (usually more risky) bonds has also risen. Higher leverage by large firms in emerging markets is also generally associated with rising risk exposure, including foreign currency and interest rate risk.

Many poorer developing economies have rapidly expanded their domestic bond markets. Public domestic debt does not carry a foreign exchange risk and can, in principle, be more directly managed by national authorities. However, in reality, domestic bond markets in poorer economies are often dominated by large foreign bondholders who easily liquidate large positions in local-currency denominated debt and repatriate earnings.

The main reason for this overall worrying trend towards rising vulnerabilities of debt sustainability in developing countries is their fast integration into highly volatile international financial markets over recent years, and in particular after the global financial crisis. While increased access to private sector finance in international markets makes it easier for capital-scarce developing countries to raise finance, it also makes them vulnerable to rapid reversals in capital inflows and exposes them to a wide array of risks that they may be insufficiently equipped to manage appropriately. Importantly, the mere access to cheap international credit does not ensure that these additional resources are channelled into productive investment, thereby bolstering long-term debt sustainability. (UNCTAD, 2015a pp. 120-132).

Strengthening the capacity of public debt management offices in developing countries to improve data collection and to manage risk associated with new debt instruments and more complex forms of development financing, such as public-private partnerships (PPP), is important to monitor public sector debt. But even the best debt management practices cannot prevent debt burdens from becoming unsustainable under conditions of severe and/or frequent exogenous shocks to an economy. It is therefore equally, if not more, important that governments in such situations can count on access to efficient and fair sovereign debt restructuring mechanisms as well as debt relief. A core objective of such mechanisms must be to allow economies in debt distress to recover economic growth fast and equitably, not least to restore future debt sustainability (UNCTAD, 2015a, pp. 132-147).