Goal 8

Decent work and economic growth

Financial intermediation plays an important facilitation role within economic systems allowing income not spent on consumption to be made available as capital for investment and allocated among different types of use in an efficient way. Financial institutions, such as banks and insurance companies, transform assets provided by savers with regard to size, risk and duration, to match them with the needs of investors. In theory, they can help to reduce information costs by producing information about potential creditors and evaluating their creditworthiness. They should also help to reduce transaction costs by facilitating the trading and management of risks and by exercising corporate governance. By diversifying investment portfolios, they should also contribute to reducing the amount of risk.

As a result, when well-functioning financial institutions are in place, investment projects that would otherwise lack sufficient financing can be realized, and higher interest is paid to savers as a return for lending their capital. Thereby, financial intermediation, if functioning properly, makes an important contribution to economic growth (Levine, 2005; Saunders and Cornett, 2008, pp. 2-8). In practice, unfortunately, the financial crisis of 2008-2009 demonstrated fundamental deficits of many banks, insurance companies, regulators and credit rating agencies in assessing risk (UNCTAD, 2015). Looking at the developments in past decades, a positive impact of financial intermediation on economic growth has been confirmed empirically by a growing volume of research. In the early stages of economic development, banks play a particularly important role, whereas in the later stages financing is to a large extent also channelled through equity markets (Demirguc-Kunt et al., 2012; Seven and Yetkiner, 2016).

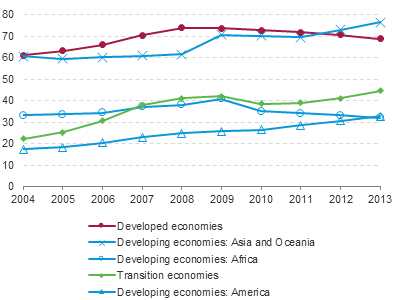

In developed economies in 2013, the loans given by commercial banks to resident private households and enterprises were on average slightly more than the equivalent of two thirds of GDP (see figure 8.9). In the developing economies of America and Africa, this ratio was only half as high, whereas in developing economies in Asia and Oceania commercial banks had an even higher propensity to provide loans to residents than in developed ones. In transition economies, the ratio of commercial bank loans to GDP amounted to slightly less than one half. Considering the developments between 2004 and 2013, the global financial crisis of 2008, which was followed by longer-lasting uncertainty, negative prospects concerning future growth and weakened trust in governments’ potentials to accommodate financial risks (IMF, 2016b), had a significant impact on commercial bank lending. This impact is particularly evident in developed economies and in Africa, where the rate of commercial bank loans has continuously declined since then, as well as in transition economies where the smooth longer-term upward trend was sharply interrupted for one year. It is noteworthy that developing economies in Asia and Oceania saw a strong expansion of commercial bank loans relative to GDP in the first year of the crisis and, after two subsequent years of stagnation, a resumption of the increasing trend. In developing economies in America, the rate of commercial bank loans to GDP increased continuously, hardly showing any sign of disturbance caused by the turbulences on the world financial markets at the end of the last decade.