Goal 12

Responsible consumption and production

The Sustainable Development Goal agenda has placed a new focus on corporate performance, behaviour and risk management, creating new demands for information on corporate reporting. Target 12.6 explicitly acknowledges the critical role that corporate sustainability reporting12.1 must play. Done properly, corporate reporting can enrich and enhance the Sustainable Development Goal monitoring framework by providing governments, enterprises, society and other stakeholders with the means to assess the economic, environmental and social impact of companies on sustainable development. Consequently, the Inter-Agency Expert Group on Sustainable Development Goal Indicators (IAEG-SDG) selected the “Number of companies publishing sustainability reports” as the indicator to measure progress towards this target.

Reporting activities that contribute to sustainability will be increasingly important to companies, as it will allow them to make customers aware of their contribution to sustainable development. Investors may also have specific interests in such reporting to assess how companies are addressing financial and reputational risks associated with sustainability challenges. But further work is needed to integrate environmental, social and governance (ESG) reporting into existing company financial and non-financial reporting models; facilitate harmonization of sustainability reporting requirements and practices; and assure the comparability and reliability of information and data provided by companies on non-financial issues. While there currently exists a myriad of international or supraregional reporting initiatives12.2, there is no universal agreement on what a sustainability reportA report published by a company or organization about the economic, environmental and social impacts caused by its everyday activities.

more is or what such a report might include12.3 in order to be defined as one. According to recent research by UNCTAD, out of the Forbes world 100 largest listed companies, 99 corporations produce some sort of ESG reporting, 51 refer to the United Nations Global Compact, 62 to the Carbon Disclosure Protocol, 10 to ISO 26000, 48 to other ISO certificates, and 72 to the Global Reporting Initiative (both G3 and G4) (UNCTAD, 2016). KPMG et al. (2016) recently published a report, “Carrot & Sticks”, that identifies almost 400 sustainability reporting instruments across 64 countries. Consequently, further work is required to develop a set of core corporate sustainability indicators and align these with overall Sustainable Development Goal monitoring.

Sustainability reporting lacks a single international institution to coordinate and harmonize its activities. The challenges associated with the absence of consistent financial reporting arrangements over the last decade illustrate why such an institution is desirable, or at the very least why it is necessary to identify areas of consistency between the different reporting frameworks to promote global consistency and convergence (International Federation of Accountants, 2013). The wide range of indicators, frameworks and guidelines issued by multiple organizations creates not only a significant duplication of effort but also a lack of clarity and a wide variety in the quality of information. The result is that corporate reports, which are often difficult to understand and compare, vary widely in terms of comprehensiveness and quality.

Agenda 2030 poses additional challenges for the harmonization, comparability and integration of related indicators. It is not yet clear what approach will be used to ensure the usefulness of corporate reports in assessing the private sector contribution towards attaining the Sustainable Development Goals. The majority of sustainability reporting requirements and initiatives are focused on listed and large private companies because they have the largest sustainability impact. But arguably a mechanism is also required for small and medium-sized enterprises; a cost-benefit analysisCost-benefit analysis is a systematic approach to estimating the strengths and weaknesses of alternatives that satisfy transactions, activities or functional requirements for a business.

more is required to determine a suitable reporting requirement.

Developing a harmonization approach to reporting on ESG information faces a number of challenges, such as those of methodology12.4; materiality12.5; burden12.6; consistency 12.7; data quality 12.8; mandatory or voluntary approaches12.9; and compliance12.10. UNCTAD promotes harmonized transparent corporate accounting and assists developing transition economies to align their corporate reporting requirements with international standards and best practices through the Intergovernmental Working Group of Experts on International Standards of Accounting and Reporting (ISAR). Sustainable reporting was incorporated into the agenda in 1993 following the United Nations Conference on Environment and Development, also known as the Rio Earth Summit. In particular, UNCTAD has developed a number of products in the area of environmental, social, governance disclosure and sustainability reporting: Integrating Environmental and Financial Performance at the Enterprise Level (UNCTAD, 2000); Guidance Manual - Accounting and Financial Reporting for Environmental Costs and Liabilities (UNCTAD, 2002); A Manual for the Preparers and Users of Eco-efficiency Indicators (UNCTAD, 2004); Guidance on Good Practices in Corporate Governance Disclosure (UNCTAD, 2006); Guidance on Corporate Responsibility Indicators in Annual Reports (UNCTAD, 2008); Best Practice Guidance for Policymakers and Stock Exchanges on Sustainability Reporting Initiatives (UNCTAD, 2014a).

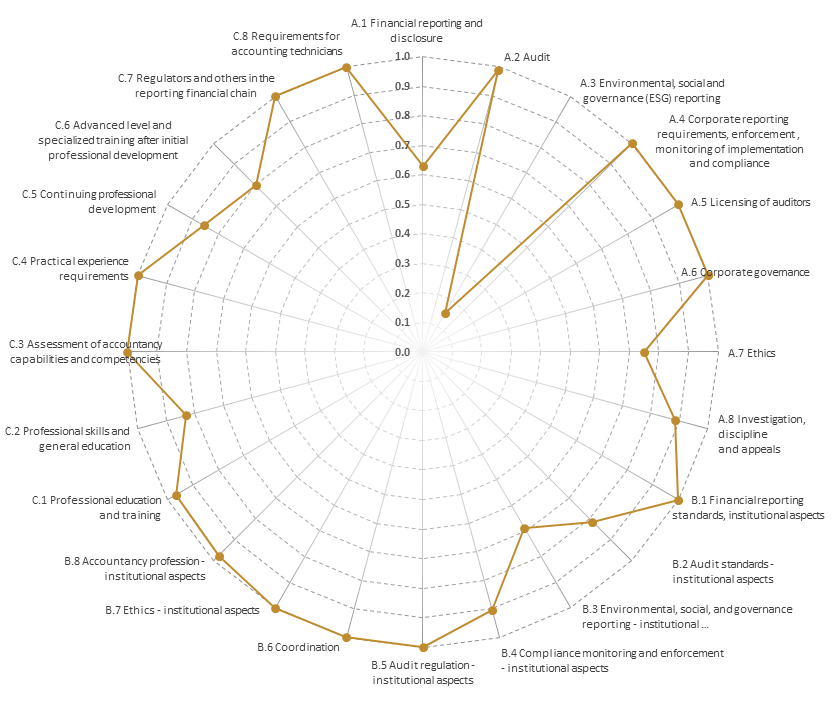

UNCTAD has also developed the Accounting Development Tool, a quantitative tool that helps countries assess their corporate reporting infrastructure using international standards and best practices as a benchmark. The Accounting Development Tool includes a separate chapter focusing on ESG reporting (see the example given in figure 12.2).

At the thirty-second session of ISAR (November 2015) member States asked UNCTAD to conduct further work in the area of sustainability reporting by identifying good practices of corporate reporting on the Sustainable Development Goals and facilitating the harmonization of sustainability reporting. To respond to the new demands posed by the Sustainable Development Goal 2030 Agenda, UNCTAD, jointly with the United Nations Environment Programme and the Group of Friends of Paragraph 4712.11, is evaluating existing reporting frameworks to identify key principles and core Goal indicators to help companies reflect their impact on their implementation, and provide a basis to monitor and assess the progress towards the Goals at a national level.