Goal 9

Industry, innovation and infrastructure

Broadening access to economic and business opportunities for small and medium-sized enterprisesNon-subsidiary independent firms that employ fewer than a given number of employees. This number varies across countries.

more (SMEs) can improve social welfare and boost national productivity. Financing is a key element of SME sector development. As national economies develop, the number of SMEs steadily increases, as does the need for access to long-term growth capital. Hence the need to develop innovative financing models that go beyond traditional bank lending to provide timely financing opportunities for SMEs according to their needs and stages of business growth (ADB, 2015).

Micro-credit is not a miracle cure that can eliminate poverty in one fell swoop.Mohammed Yunus (Yunus, 2003)

Two indicators have been selected by IAEG-SDG to measure progress towards target 9.3. The first indicator, the Proportion of small-scale industries in total industry value added

was selected as micro and small establishments or enterprises play an important role in the economy. Often established with a relatively small investment, SMEs are an important source of direct employment and self-employment, but also indirectly through purchases of local raw materials.

The second indicator, the Proportion of small-scale industries with a loan or line of credit

, was selected as micro and small-scale firms often have limited access to funding and financial services. Unfortunately, in both cases, but in particular the latter case, there are few comparable data publically available to populate these indicators. Thus, the need for improved data on SME financing is obvious (ADB, 2015; United Nations, 2015).

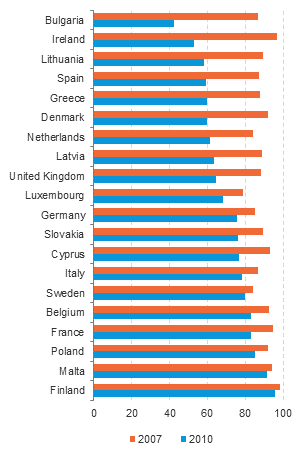

Although comparable data on loans to firms are not available at a global level, several member States in the European Union conducted a study on the challenges of accessing finance being faced by firms following the financial crisis of 2008/09. These data, the first official statistics of their kind, provide a valuable insight on the funding constraints faced by SMEs in the aftermath of the crisis. The financial crisis was felt most acutely in developed economies and the fallout for SMEs in terms of accessing finance is evident from figure 9.11. As banks concentrated on repairing their balance sheets, loan finance available to SMEs tightened up significantly. This is particularly evident in countries such as Bulgaria, Greece, Ireland, Lithuania and Spain, where successful loan applications fell sharply9.4.

The loan patterns identified in the European Union are not unique to Europe. In Asia, a similar trend in the decline of bank loans to SMEs since the 2008/09 global financial crisis has been identified. In 2014, bank loans to SMEs accounted for almost 19 per cent of total bank lending for Asia SME Finance Monitor countries9.5, indicating continuing problems to access bank credit (ADB, 2015). ADB has also noted there are some concerns regarding the negative impact of Basel III9.6 on SME lending, saying these new measures may constrain banks from providing long-term credit for enterprises, and may limit financing options, including trade finance availability.

This difficulty may be exacerbated in developing countries where many SMEs lack financial documentation, making lenders reluctant to lend owing to the greater risk. But of course, finance is a necessary but not sufficient condition for small firms to develop and thrive. Other factors like entrepreneurial skills, infrastructure and supportive macroeconomic and trade policy must also be in place (Chowdhury, 2009).

Microenterprises face similar and additional challenges to SMEs when trying to access financial intermediation.

However, the constraints of accessing financial services can be overcome by the use of mobile credit made available via mobile phones. Systems such as M-Pesa9.7 in Kenya or bKash in Bangladesh have allowed millions of entrepreneurs who do not have bank accounts to access financial services (Radalet, 2015; Rundle, 2015; Quadir, 2014). Technology is not limited to providing payment and transfer facilities, as microenterprises can also use mobile technology to access microloans. The Grameen Bank in Bangladesh, founded by Nobel laureate Professor Yunus, has developed a specialized group-based (solidarity) approach to microfinance lending, thus overcoming the traditional constraints of lack of collateral and financial records by assuming joint liability and issuing very small loan amounts.