Goal 10

Reduced inequalities

Economies are particularly vulnerable to financial instability when international capital flows are mainly of a short-term nature. Unlike the foreign capital that is used in fixed capital formation, short-term flows are normally used for the acquisition of financial assets, real estate investments or consumption credit, directly or through the intermediation of domestic financial systems. Such flows are particularly prone to boom-and-bust cycles, depending mainly on events in the more developed economies. They exacerbate the fragility and vulnerability of domestic financial systems and lead to unsustainable current-account deficits. Further, the drying up or reversal of such inflows has frequently resulted in pressures on the balance of payments and on the financing of both the private and public sectors, and has led to recurrent debt crises and protracted economic depressions.

The very high costs caused by international financial instability explain why an increasing number of countries have resorted to capital management policies, including inward and/or outward capital controls. There is indeed a strong case for governments to manage capital flows by seeking to influence not only the amount of foreign capital movements, but also their composition and use. Such a pragmatic and selective approach to capital flows, rather than unrestricted openness or a complete ban, could help maximize policy space within a given development strategy and given existing international institutional arrangements. Such measures are allowed by the International Monetary Fund (IMF) Articles of Agreement, and their legitimacy has been further corroborated by other international institutions. However, their implementation requires non-negligible administrative capacities and resources at the national level. In addition, their effectiveness is also limited, given that private speculative capitals may try to circumvent controls by many different ways.

This is one reason why national efforts should be complemented by a global approach, in other words - a global solution to a global problem. Target 10.5 therefore aims to reduce global financial instability through improved monitoring and regulation. IAEG-SDG has proposed a set of financial soundness indicators

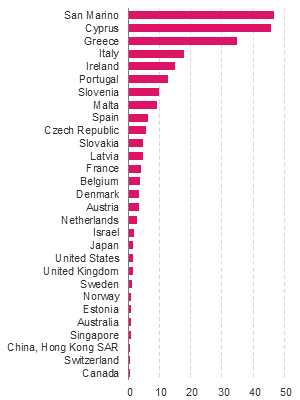

as the best way to measure implementation progress. Unfortunately, at the time of writing no further information was available on what exact indicators IAEG-SDG was proposing. However, the IMF Financial Soundness Indicators are probably a good gauge of the type of dashboard we might expect10.17. The impact of the 2008 financial crisis is evident in the data - in particular for the so-called advanced economies

where, for example, the percentage of non-performing bank loans remains very high10.18 (see figure 10.4).

One proposal for discouraging speculative capital flows without hampering long-term financing is to establish a small fee for international financial transactions: small enough to be irrelevant for financial operations linked to real investment, but sufficient to undermine the benefits expected from very short-term speculative operations. The taxation of international currency transactions was initially proposed by the economist James Tobin in 1972 and has been generically known since then as the Tobin taxAn excise tax assessed on currency conversions.

(New Rules for Global Finance Coalition, 2003; Palley, 2003).

more

Such a tax could deliver a number of positive outcomes. First, it would discourage an activity that has proved to be detrimental to economic stability and development. Second, it represents a progressive tax on wealthy financial actors. Third, it sets similar rules of the game for all the countries participating in such a system and allows for a centralized and efficient system for collecting the tax - for instance, during the clearing or settlement process - which would be easier to apply than most measures that can only be implemented at national level. Last but not least, international financial transactions are so large that even a very small taxation rate would generate significant fiscal resources, which could either be distributed among the participating countries or used to finance other global public goods or development programmes10.19.

Several countries have already established different kinds of taxes on financial transactions. However, the most relevant initiative is the Financial Transaction Taxation (FTT) proposed by the European Commission in 201110.20 and endorsed by 11 countries in 201310.21. This regional agreement proposes to set a tax of 0.1 per cent on stock and bond trades and 0.01 per cent on the notional value of derivatives. Trading platforms and clearing houses would collect the taxes and pass the revenue to national tax authorities. It was estimated that, if applied to the whole European Union, the tax would generate €57 billion annually (Hemmelgarn et al., 2015); the tax take would fall to between €30 billion and €35 billion (Mehta, 2013; Hemmelgarn et al., 2015) if the tax only applied to the 11 countries that in principle agreed to adopt the system.

If applied among most of the major countries of the eurozone, FTT will provide valuable experience on the international taxation of financial flows. If implementation of FTT is successful, extending it to other countries and regions, or replacing it with a similar, but multilateral system could then be considered. A global FTT system could generate a very significant amount of resources, similar if not larger than that actually mobilized through official development assistance (ODA). Those resources, based on globalized financial flows, could be made available for the financing of global public goods, such as environmental protection or sustainable development.