Goal 17

Partnerships for the goals

A public - private partnership or PPP is a contract between a government and a private company under which the private company finances, builds and operates some element of a service that was traditionally considered a government domain. Definitions of PPPs vary considerably, reflecting different institutional arrangements and conceptual understandings17.88. PPPs have been used widely over the past 20 years, and are currently seeing a revival of interest in the context of financing the 2030 Development Agenda. For more details refer to chapter 6 of the Trade and Development Report 2015 (UNCTAD, 2015a).

PPPs are typically employed to implement infrastructural projects when public budgets are constrained. Properly managed, they may also improve public service efficiency through technical expertise provided by the private sector (ECLAC, 2015). But there can be downsides and hidden or unexpected fiscal and other costs. Benchmarking PPP performance compared with alternatives, such as traditional public procurement, has not always been done properly. Thus the role of public sector finance should not be underestimated (UNCTAD, 2015a). A cautious approach is needed if PPPs are to deliver the expected development benefits and to avoid or minimize the potential costs such partnerships can generate (Independent Evaluation Group, 2014).

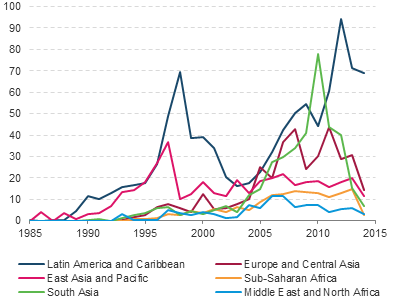

In 2013, PPP funding for infrastructure projects in developing countries amounted to approximately US$159 billion, having recovered after the economic and financial crisis of 2008/2009 but falling sharply from a peak in 2012 (UNCTAD, 2015a). Despite the recent downturn, the use of PPPs has increased markedly since their introduction in the 1980s (figure 17.12), recovering from setbacks following the Latin American and Asian crises, as well as Enron and other corporate scandals that affected even those countries that had previously been successful in attracting capital (World Bank, 2009). Their use in developed countries has also shown a broad overall increase, and again reflects sensitivity to external shocks and the broader economic cycle. However, in Europe the value of PPPs was around €13 billion in 2012, the lowest in at least 10 years. These recent trends point to the challenges that lie ahead. Never has the cost of debt been lower and yet it is increasingly difficult to finance new infrastructure investment, especially when equity commitment is a requirement (Helm, 2010).

PPP investment has been concentrated in relatively few countries and sectors. Almost 60 per cent of the total private participation in projects recorded in developing countries was in (by order of magnitude) China, Brazil, the Russian Federation, India, Mexico and Turkey. This is an indication that PPP investors are not dissimilar from other institutional investors, preferring large and dynamic markets to the more vulnerable economies where financing needs are greatest. Among developing regions, Latin America has traditionally hosted the largest share of PPPs and still accounted for 45 per cent of the total in 2013. Only 10 per cent of the total went to Africa, although in sub-Saharan Africa investments have been steadily rising (primarily because of investments in telecoms) (UNCTAD, 2015a).

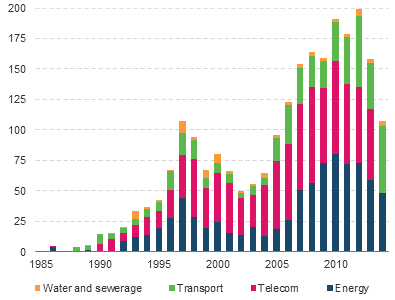

PPP investments have been concentrated in relatively few sectors, with telecoms accounting for 37 per cent of the total, or US$58 billion, in 2013, and energy for 37 per cent of the total, or US$59 billion (see figure 17.29). Water and sanitation are among the most needed infrastructure services to relieve human suffering (See Goal 6), and yet they are the least likely to be financed through this method, having received a mere US$3.5 billion in 2013 (UNCTAD, 2013c). Indeed, most commercial interest has been directed to ICT and energy-related activities, while socially challenging sectors attracted almost no private activity (Africa Infrastructure Country Diagnostic, 2010). PPPs also appear more likely to emerge in brownfield projects17.89 than in completely new greenfield projects or risky transformative activities such as those related to climate change (World Economic Forum, 2014).

Thus, despite the growth in the use of PPPs, State investment in infrastructure development remains important, especially at times of uncertainty. Estimates of the share of public investment in infrastructure vary from anywhere between 75 per cent and 90 per cent (Estache, 2010; Briceño-Garmendia et al., 2008; Hall, 2015). Even in the European Union, PPPs on average contribute a very small share to total infrastructure investment. In developing countries, governments financed around 70 per cent of infrastructure investment during the period 2000−2005, rising to 90 per cent for the lowest income countries17.90. To a large extent, this reflects the very nature of infrastructure. As the World Bank has noted (World Bank, 2009, p.78), many governments see the private sector as a solution. However, private financing, while offering additional resources, does not change the fundamentals of infrastructure provision: customers or taxpayers (domestic or foreign) must ultimately pay for the investments, and cost-covering tariffs (and well-targeted subsidies) remain the centrepiece of all sustainable infrastructure provision, public or private

.

As a result, even with PPPs, public finance remains critical. Of the total investment in developing countries broadly described by the World Bank as PPPs, public debt and equity accounted for 67 per cent and private debt and equity accounted for the remaining (Mandri-Perrott, 2014). Moreover, these data relate only to the phase before projects are operational, after which contingent liabilities and other charges generally add considerably to the total public costs.